Retirement Planning | Generate Retirement Income

Any successful journey requires detailed planning. When the stakes are high, winging it isn’t an option. We start with our proprietary Stenger Retirement Planning Process.

5 Steps to a Successful Retirement

Our proprietary 5-Step Retirement Navigation Process starts with an assessment of your future goals. Your Stenger financial advisor will take an inventory of your income, projected retirement expenses, assets and liabilities and create a customized financial plan that addresses your specific needs. Because Stenger Family Office operates as a multi-family office, our financial advisors will work directly with our in-house team of accountants and estate planning attorneys to create a comprehensive plan that addresses all aspects of your financial life.

Step #1:

Income & Expenses

Retirement planning solves the key problem of paying expenses on a fixed income. Your Stenger Financial Advisor will add up your expected income, subtract your monthly expenses, calculating your retirement income gap. This income gap will be compared against your assets and liabilities to determine if you have enough saved to retire.

Step #2:

Assets & Liabilities

After calculating your annual retirement income gap, your Stenger financial advisor will take an inventory of your investable assets and the potential amount of additional income these assets can generate. In general, we want our clients to be as debt free as possible approaching retirement.

Step #3:

Investment Management

Many investment portfolios are created with a risk questionnaire, asking investors how much risk they can tolerate. While this is an important component of portfolio construction, we believe investors should implement a goals-based financial plan, not risk-based. A goals based plan helps you address the most important question - “Will I run out of money during retirement?”

Step #4:

Tax Strategy

Often times, tax planning and strategy go overlooked when creating a financial plan. While there are no quick and easy ways to save money on taxes in any given year, there are substantial savings that can be achieved through long range tax planning and preparation. As a multi-family office, we employ an in-house team of accountants and CPAs to create a tax efficient plan alongside your financial advisor.

Step #5:

Estate Planning

Passing down your assets and legacy to the next generation is an important component of retirement planning. At the very least, not leaving a mess to your children and grandchildren can be achieved through thoughtful estate planning strategies coordinated alongside your financial and tax strategies.

Stenger Retirement Planning Process

-

![A person wearing a beanie, jacket, and backpack walking on a narrow ledge between tall rocky cliffs overlooking the ocean with grass and rocks on the cliffs.]()

Identify Your D.O.S.

D.O.S. stands for Dangers, Opportunities and Strengths. Your Stenger financial advisor will help you identify what strengths you already have, what you’re most looking forward to about the future, and uncover some blind spots and risks you may not have yet considered.

-

![Blueprint or wireframe sketch of a website layout or design with sections labeled 'Présentation,' 'La Puissance,' 'Formation,' and 'Carrières,' featuring handwritten notes and diagrams.]()

Customized Financial Plan

As your financial advisor, we will create a comprehensive and customized financial plan that helps you answer one central question - “Can you live the rest of your life without running out of money?”

-

![A tall bookshelf filled with old leather-bound books, with a metal ladder leaning against it for reaching higher shelves.]()

Tax & Estate Planning

Taxes and estate planning are often overlooked during the planning process. Your Stenger financial advisor will work closely with a CPA or attorney of your choosing or introduce you to one of our in-house tax planning & preparation experts and estate planning attorney.

-

![Close-up of a digital dashboard displaying various graphs, metrics, and scores, including a quality score of 9.38, with line charts and other analytical data.]()

Investment Management

We believe your money should be invested on a customized plan that matches your financial plan, not a cookie cutter portfolio that takes on excessive risk. During the planning process, your financial advisor will recommend an investment portfolio that helps you reach your goals while minimizing unnecessary risk.

Your Customized Retirement Plan

Stenger Family Office financial advisors will help you create a plan that achieves your goals and has a high chance of success given a variety of potential market environments.

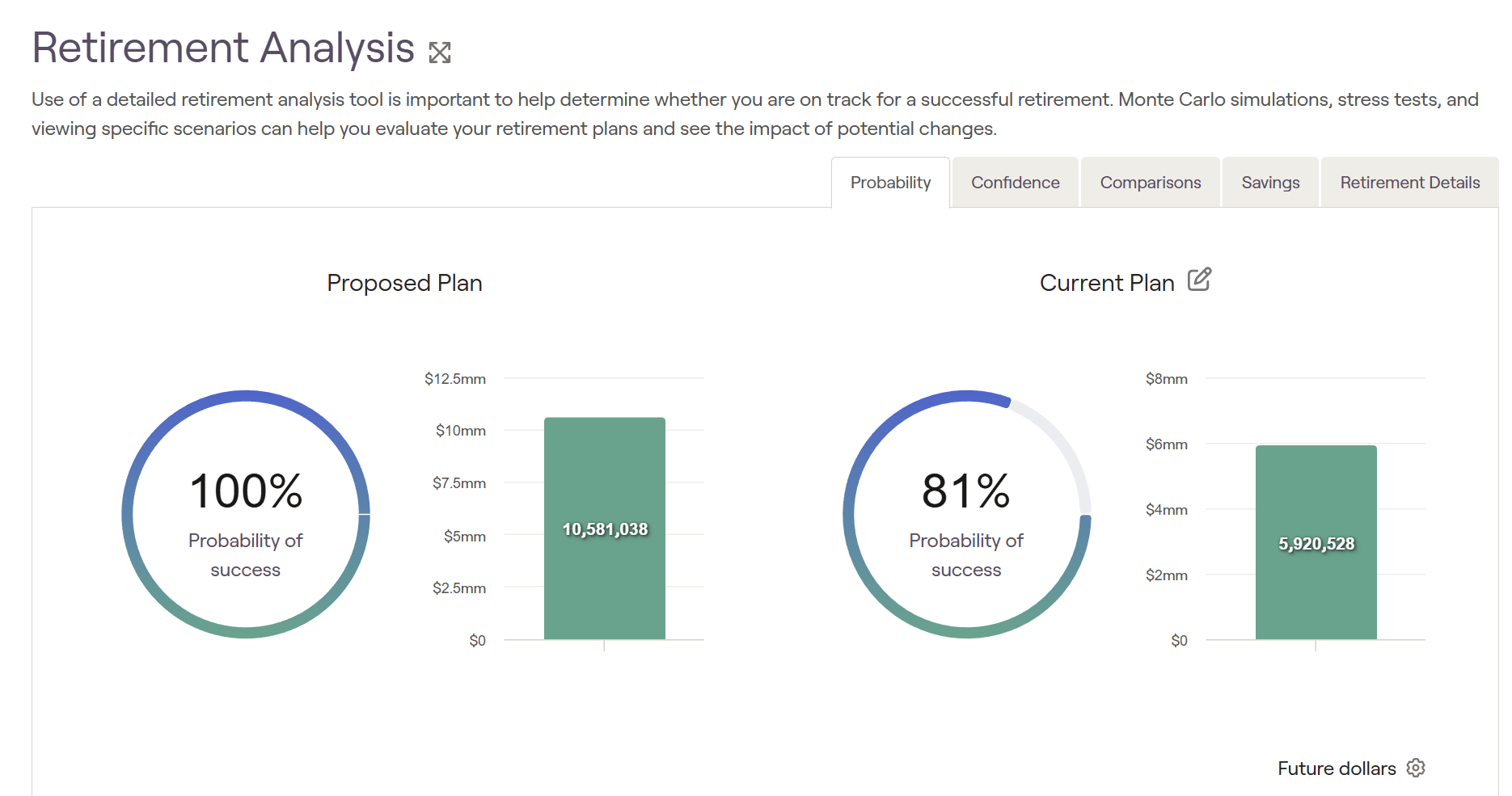

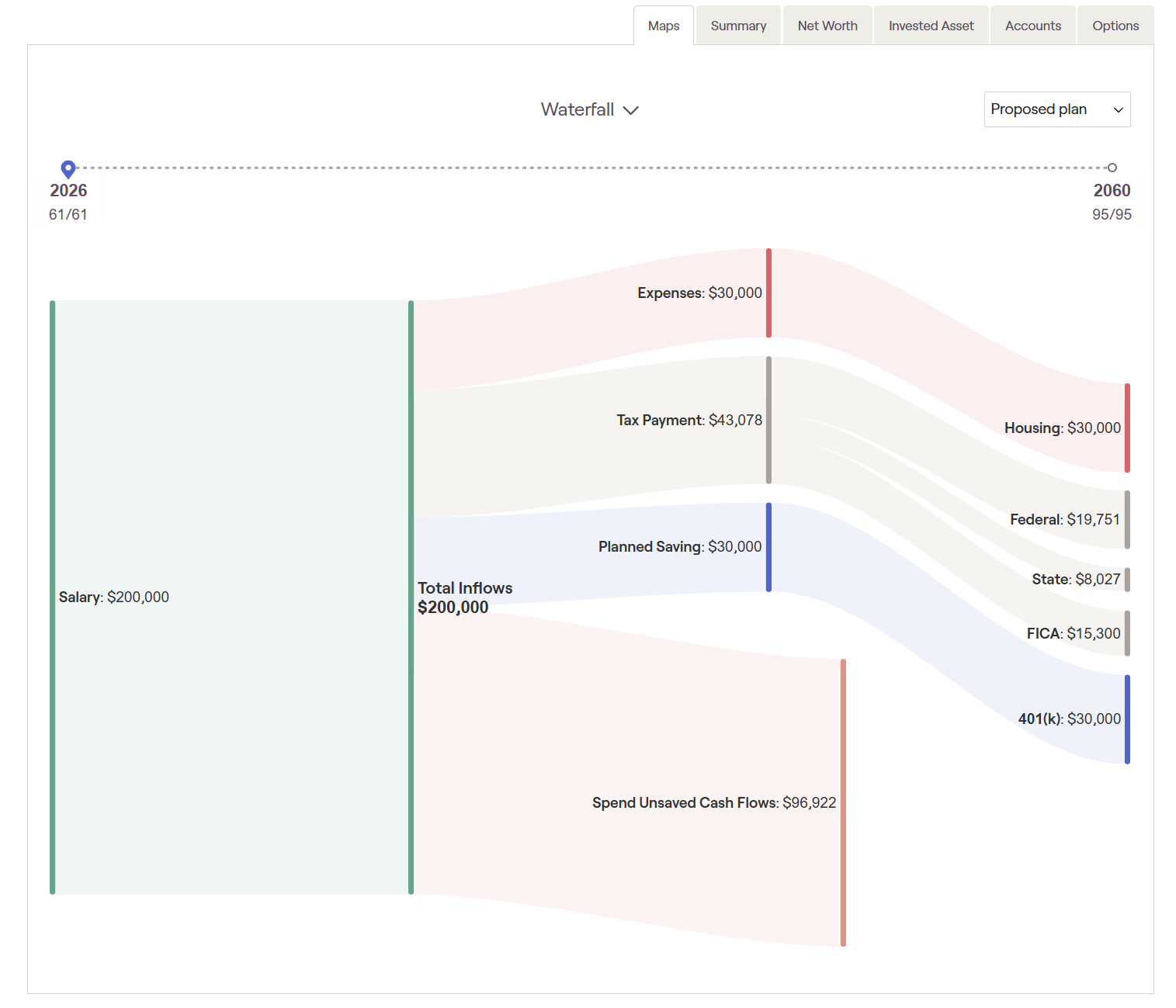

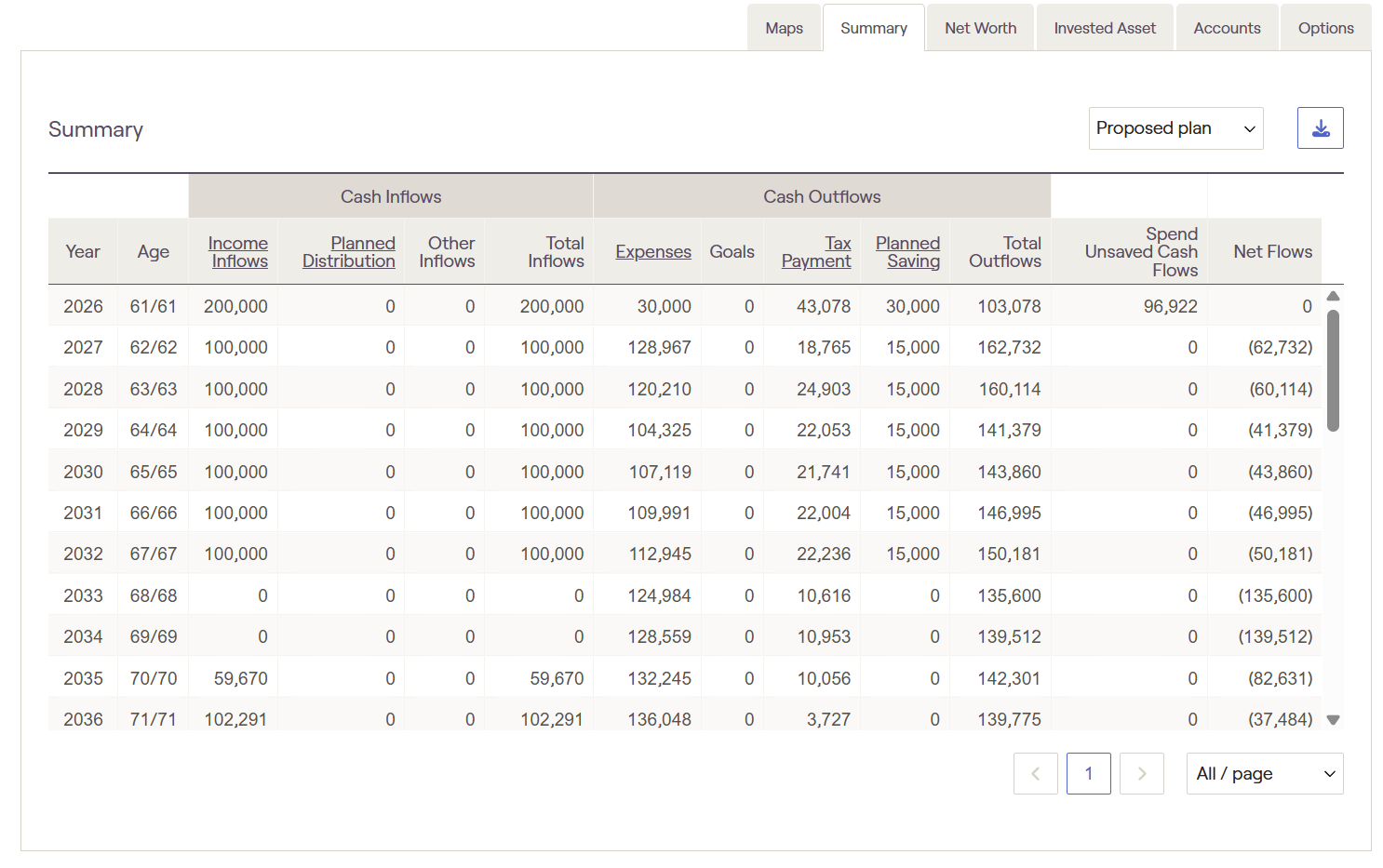

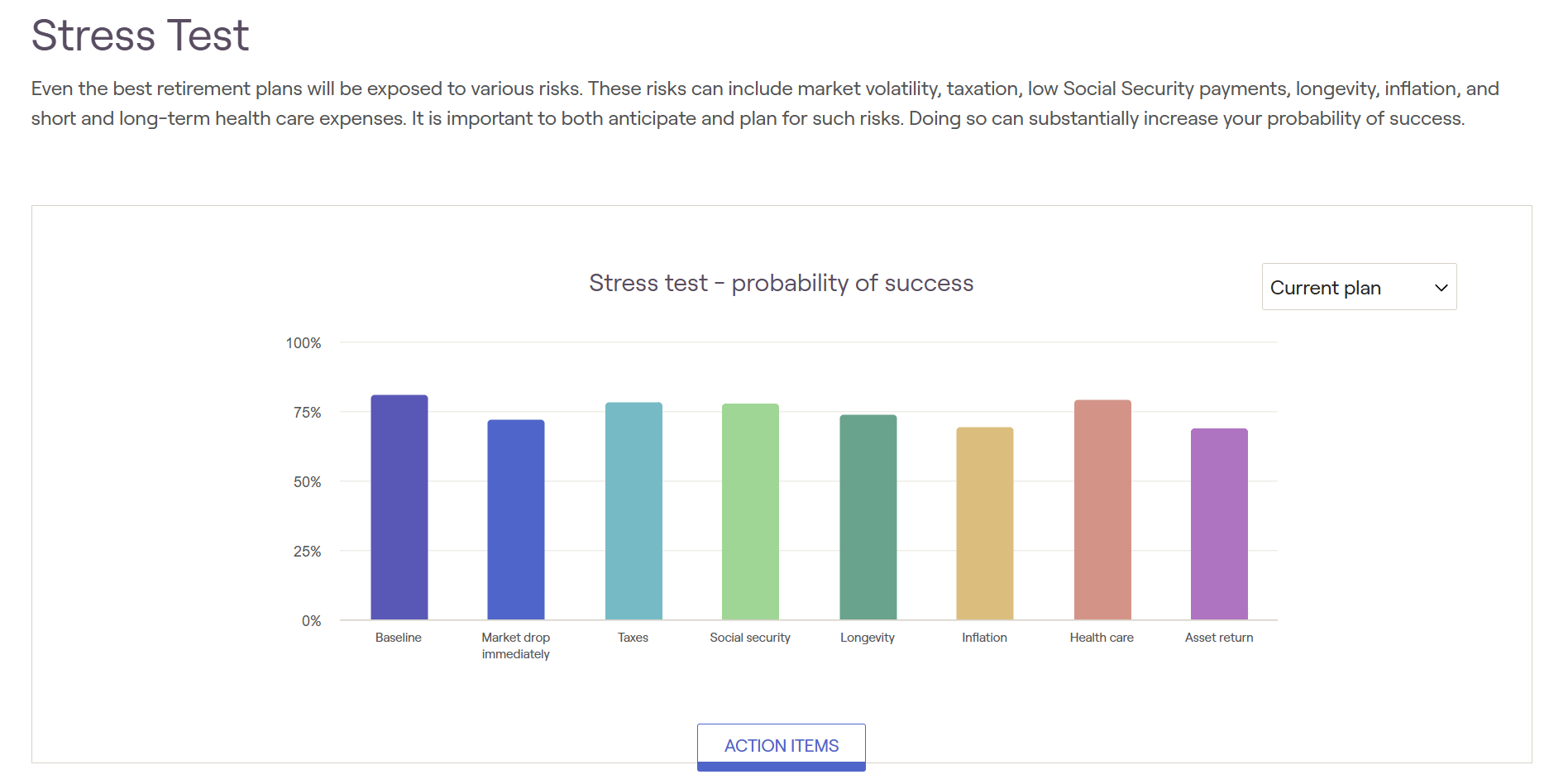

Our retirement process begins with an inventory of your assets, liabilities, income and expenses, and what we expect you’ll need to maintain your lifestyle and accomplish your goals during retirement. The most important part of retirement planning is developing your plan to generate income from investments and other fixed sources.

The screenshot above is an example of a Monte-Carlo simulation, taking into account return assumptions, sequence of returns in retirement, and a variety of other factors. Stenger financial advisors will build your investment plan based on what your goals based plan calls for. We do not build risk based investment portfolios, but rather goals based portfolios that align with your needs.

Retirement Cash Flow Projections

Retirement cash flow planning is the process of making sure your money lasts as long as you do. Instead of focusing only on how much you save, it looks at how income and expenses will line up month by month and year by year once you stop working. Good planning helps retirees maintain their lifestyle, handle surprises, and reduce stress about running out of money.

1. Understanding Retirement Expenses

The first step is estimating expenses. Some costs may drop in retirement, such as commuting or work-related spending, while others often rise, especially healthcare, insurance, and leisure activities. Expenses usually change over time:

Early retirement: Travel and hobbies may increase spending.

Mid-retirement: Spending often stabilizes.

Later years: Healthcare and support costs may grow.

Planning for these phases makes cash flow more realistic.

2. Identifying Income Sources

Retirement income usually comes from multiple sources, such as:

Pensions or annuities

Government benefits (like Social Security, depending on country)

Investment withdrawals (stocks, bonds, mutual funds)

Part-time work or rental income

Each source has different timing, reliability, and tax treatment, which affects how cash flows throughout the year.

3. Matching Income to Expenses

A key goal is to align reliable income with essential expenses (housing, food, utilities, healthcare). Guaranteed or predictable income is best used to cover necessities, while more flexible or variable income can fund discretionary spending like travel or hobbies.

4. Withdrawal Strategies

For investments, deciding how much to withdraw and when is critical. Withdrawing too much early can increase the risk of running out of money later. Common strategies include:

Using a percentage-based withdrawal

Drawing from taxable accounts first, then tax-deferred accounts

Keeping short-term spending money in safer assets to avoid selling investments during market downturns

5. Managing Risks

Retirement cash flow planning must account for risks such as inflation, market volatility, and longer-than-expected lifespan. Diversifying income sources, adjusting spending when needed, and reviewing the plan regularly help manage these risks.

6. Ongoing Review and Adjustment

Retirement is not static. Expenses, health, markets, and personal goals change over time. Reviewing cash flow plans regularly ensures they stay aligned with reality and allows for timely adjustments.

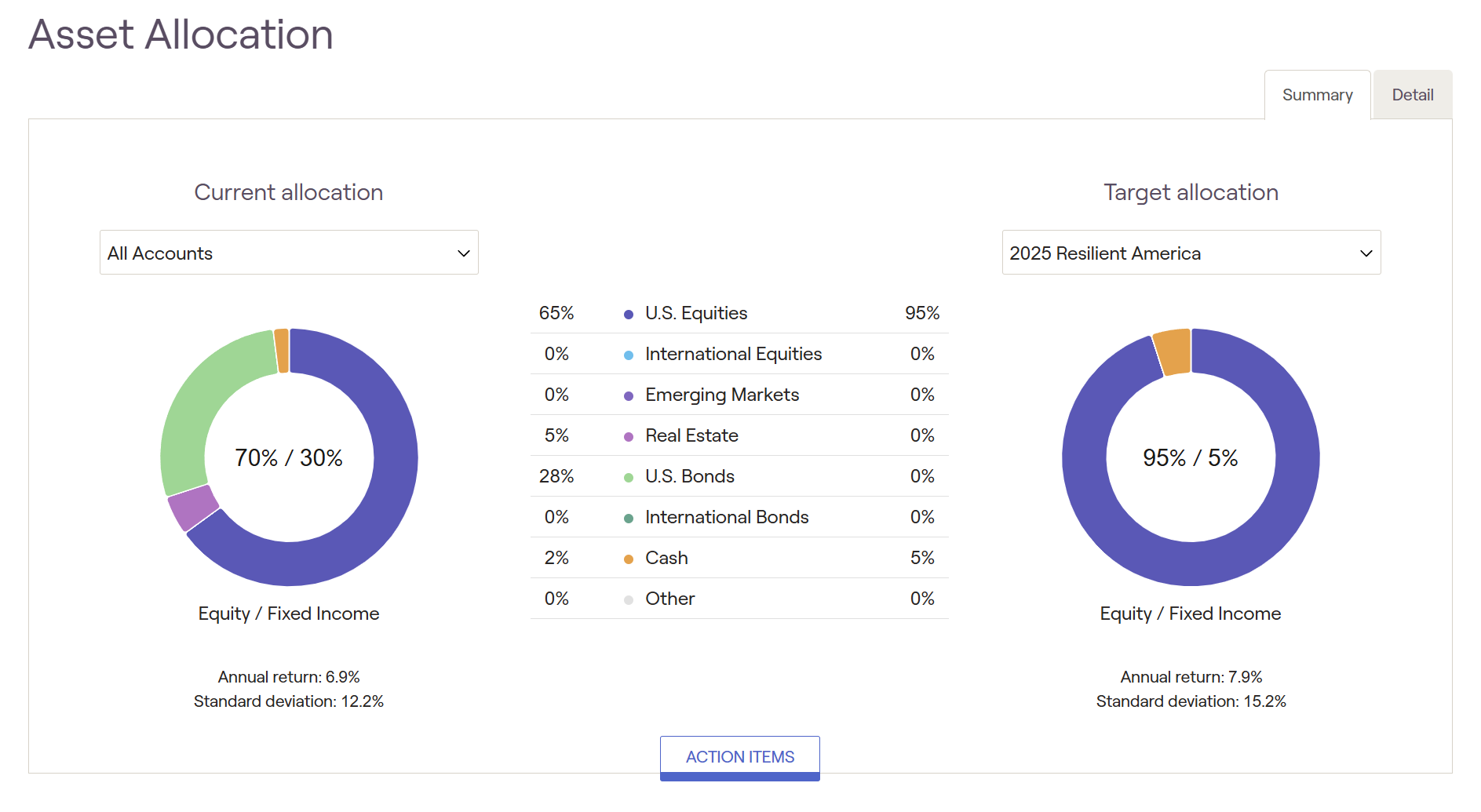

Investing During Retirement

Asset allocation during retirement is the strategy of dividing investments among different asset classes—such as stocks, bonds, and cash—to balance growth, income, and risk. While accumulation years focus heavily on growth, retirement requires a more balanced approach that supports regular income while protecting against market downturns and inflation.

1. Shifting Goals in Retirement

In retirement, the primary investment goals usually include:

Generating reliable income

Preserving capital

Maintaining enough growth to outpace inflation

Because retirees are drawing from their portfolios, large market losses can be harder to recover from than during working years.

2. Role of Major Asset Classes

Equities (stocks): Provide long-term growth and inflation protection. Even in retirement, holding some equities is important to support longer life spans.

Fixed income (bonds): Offer income and stability, helping reduce portfolio volatility.

Cash and cash equivalents: Provide liquidity for near-term expenses and help avoid selling investments during market downturns.

Alternative assets (optional): Real estate or other alternatives can add diversification, but they should be used carefully due to liquidity and risk considerations.

3. Time-Based Allocation Approach

Many retirees use a “bucket” or time-segmentation strategy:

Short-term bucket: Cash and short-term bonds to cover 1–3 years of expenses.

Mid-term bucket: Bonds and conservative investments for the next several years.

Long-term bucket: Growth-oriented assets like stocks for later retirement years.

This approach helps match assets to spending timelines and reduce emotional reactions to market swings.

4. Managing Sequence-of-Returns Risk

Poor market returns early in retirement can significantly impact long-term outcomes. To manage this risk, retirees often:

Keep sufficient safe assets for early withdrawals

Adjust spending during market downturns

Rebalance portfolios regularly to maintain target allocations

5. Adjusting Asset Allocation Over Time

Asset allocation in retirement is not static. As retirees age, they may gradually reduce risk, but this should be balanced against the need for growth. Regular reviews help ensure the portfolio still aligns with spending needs, health, and life expectancy.

6. Tax Considerations

Different asset classes may be better suited for different account types. For example, income-producing assets may fit better in tax-deferred accounts, while growth assets may be more efficient in taxable accounts. Thoughtful placement can improve after-tax cash flow.

Meet the Financial Advisors

-

Nick Stenger

CEO & Financial Advisor

Nick Stenger is the Chief Executive Officer and financial advisor at Stenger Family Office. Nick is a 7th generation Naperville, IL resident where he lives with his wife Jamie and son Jack. Prior to launching Stenger Family Office, Nick was a Senior Vice President and financial advisor at Morgan Stanley Wealth Management. Nick helped lead the team’s growth to become one of Morgan Stanley’s largest wealth management teams. In 2023, Nick and the team were named one by Forbes as a Best-In-State Wealth Management team in Illinois. Prior to Morgan Stanley, Nick worked at Invesco PowerShares, a $1 trillion asset manager in Atlanta, GA and PricewaterhouseCoopers, LLP (PwC) in Chicago, IL. Nick is a graduate of the Quinlan School of Business at Loyola University Chicago with degrees in accounting and finance.

-

Chris Jordan, CPA, MST

Chief Financial Officer

Chris Jordan is Chief Financial Officer and Head of Tax at Stenger Family Office. Chris leads the Stenger tax team and assists family office clients with tax preparation and advisory services.

Chris is a Certified Public Accountant and specializes in business tax preparation, individual tax preparation, partnerships, estate taxation, and high net worth family taxes. Prior to Stenger Family Office, Chris was a Tax Manager at Porte Brown, a midsize accounting firm in the Chicago suburbs.

Chris earned his BA in Accounting from Augustana College and his Masters of Science in Taxation from the Carl H. Lindner College of Business at the University of Cincinnati.

-

Audrey Feldpausch, CFP®

Vice President, Financial Advisor

Audrey Feldpausch is a Vice President and Financial Advisor with Stenger Family Office. Audrey leads the team’s financial planning practice and also is a member of the Stenger Family Office Investment Committee. Audrey is a CERTIFIED FINANCIAL PLANNER™ and completed her CFP® training through Northwestern University in Chicago, IL. Prior to Stenger Family Office, Audrey worked at UBS Wealth Management and Timothy Financial, a financial planning firm in the Chicago suburbs. Audrey is a graduate of Hillsdale College where she earned her B.A. in Economics. Audrey and her husband live in the Chicagoland area.

Our multi-family office approach helps simplify and organize your financial life.

Our Office Locations

-

Naperville Financial Advisor

Naperville Financial Center

400 E. Diehl Road

Suite 550

Naperville, IL 60563 -

Chicago Financial Advisor

150 N. Riverside Plaza

Suite 1950

Chicago, IL 60606 -

Houston Financial Advisor

City Place

1700 City Plaza Drive

Suite 440

Spring, TX 77389 -

Baton Rouge Financial Advisor

City Plaza

445 North Blvd

Suite 570

Baton Rouge, LA 70802

Fiduciary Financial Advisor Naperville, Chicago, Houston & Baton Rouge.

Take the next step with our team of experienced financial advisors, financial planners, tax accountants, estate planning attorneys and insurance specialists. The first step in the Stenger Retirement Planning Process is to create a comprehensive financial plan. We can meet with you in-person at our local Naperville, IL, Houston, TX, Baton Rouge, LA offices or at a location that works best for you.

How to Find the Right Retirement Financial Planner for Your Future

Retirement is the largest financial transition of your life. Finding the right retirement financial planner isn't just a smart move — for most people, it's the single most consequential financial decision they'll ever make.

Whether you're five years from retirement or already in it, working with a dedicated retirement financial planner can be the difference between running out of money in your 80s and living comfortably for the next three decades. But with thousands of advisors competing for your attention, knowing how to evaluate and choose a retirement financial planner takes more than a Google search.

This guide walks you through everything you need to know — from the credentials to look for, to the questions that separate great retirement financial planners from mediocre ones.

Key facts:

Americans have an average $1.46 million retirement savings gap

33% of Americans have no retirement savings at all

The average retirement lasts over 20+ years

What does a retirement financial planner actually do?

A retirement financial planner is a financial professional who specializes in helping people plan for and live through retirement. Unlike a general financial advisor who might focus on wealth accumulation or insurance products, a retirement financial planner takes a comprehensive view of your entire financial picture — from when you can afford to stop working, to how much you can safely spend each year once you do.

The core services a retirement financial planner provides typically include:

Retirement income projections and "can I retire?" analysis

Social Security optimization — determining the ideal age to claim

Medicare and healthcare cost planning

Tax-efficient withdrawal strategies from IRAs, 401(k)s, and taxable accounts

Required Minimum Distribution (RMD) planning

Estate planning coordination with your attorney

Long-term care insurance review and planning

Inflation and sequence-of-returns risk management

Credentials that matter when choosing a retirement financial planner

The financial advisory industry has more designations than almost any profession, and not all of them carry equal weight. When evaluating a retirement financial planner, these are the credentials that signal genuine expertise:

CFP® — Certified Financial Planner

The most recognized credential in comprehensive financial planning. Requires 6,000+ hours of experience, a rigorous board exam, and ongoing education. Most high-quality retirement financial planners hold this designation.

RICP® — Retirement Income Certified Professional

Granted by The American College of Financial Services, this designation is specifically focused on retirement income — making it particularly relevant when vetting a retirement financial planner.

CFA® — Chartered Financial Analyst

A highly rigorous investment-focused credential. More relevant if your primary concern is portfolio management alongside retirement planning.

ChFC® — Chartered Financial Consultant

Similar depth to the CFP® with additional coursework. A solid indicator of comprehensive financial planning knowledge in a retirement financial planner.

Fee structures: how your retirement financial planner gets paid

How a retirement financial planner is compensated directly shapes the advice they give you. Understanding fee structures is non-negotiable before committing to anyone.

Fee-only: Paid directly by you — hourly, flat fee, or a percentage of assets under management. No commissions. This is generally the most conflict-free structure for a retirement financial planner.

Fee-based: Charges fees AND earns commissions on products sold. Can still be excellent, but requires careful vetting to ensure recommendations aren't product-driven.

Commission-only: Earns money solely through selling financial products — insurance, annuities, mutual funds. Not inherently unethical, but the conflict of interest is significant for retirement financial planning.

Subscription/retainer: A growing model where you pay a flat monthly or annual fee for ongoing access to your retirement financial planner. Popular with newer advisory firms serving younger retirees.

Questions to ask before hiring a retirement financial planner

A great retirement financial planner welcomes hard questions. These are the ones that matter most:

"What percentage of your clients are at or near retirement, and what does a typical client look like?"

"How do you develop a retirement income strategy — what frameworks or methodologies do you use?"

"How do you handle Social Security claiming decisions and Medicare enrollment?"

"What happens to my plan if markets drop significantly in my first three years of retirement?"

"How are you compensated, and can you show me a full disclosure of all fees?"

"Will you be my primary point of contact, or will I be handed to a junior associate?"

How much does a retirement financial planner cost?

The cost of working with a retirement financial planner varies significantly by model and scope. A comprehensive retirement financial plan typically runs between $2,000 and $25,000 as a one-time flat fee. Ongoing advisory relationships structured as a percentage of assets under management typically range from 0.5% to 1.5% annually. Hourly retirement financial planners generally charge $200 to $1,500 per hour.

The right question isn't "how do I find the cheapest retirement financial planner?" — it's "am I getting enough value to justify the cost?" A retirement financial planner who helps you optimize your Social Security strategy alone can add tens of thousands of dollars in lifetime income. The fee pays for itself many times over when the advice is sound.

The bottom line

Retirement planning is too important to wing it, and too complex to hand off to someone without the right expertise. A qualified retirement financial planner brings both — the technical knowledge to optimize every dimension of your financial picture, and the experience to help you avoid the mistakes that can quietly devastate a retirement portfolio.

Start with credentials (CFP® at minimum), verify the fiduciary standard in writing, understand exactly how your retirement financial planner is compensated, and use the NAPFA or CFP Board directory to build your shortlist. The right retirement financial planner is out there. The time you spend finding them is among the best-invested hours of your financial life.

Contact Us

Naperville Financial Advisor

400 E. Diehl Road

Suite 550

Naperville, IL 60563

Chicago Financial Advisor

150 N. Riverside Plaza

Suite 1950

Chicago, IL 60606

Houston Financial Advisor

1700 City Plaza Drive

Suite 440

Spring, TX 77389

Baton Rouge Financial Advisor

445 North Blvd

Suite 570

Baton Rouge, LA 70802

Phone

(630) 912-8431