Term life insurance vs. whole life insurance - which one is better?

Nobody likes thinking about life insurance. But choosing the wrong policy — or skipping it altogether — can leave the people you love in a genuinely difficult spot. The good news: this decision is simpler than the industry makes it seem. At its core, the term vs. whole life debate comes down to one question — do you want pure protection, or protection plus savings? Both are legitimate answers, depending on where you are in life.

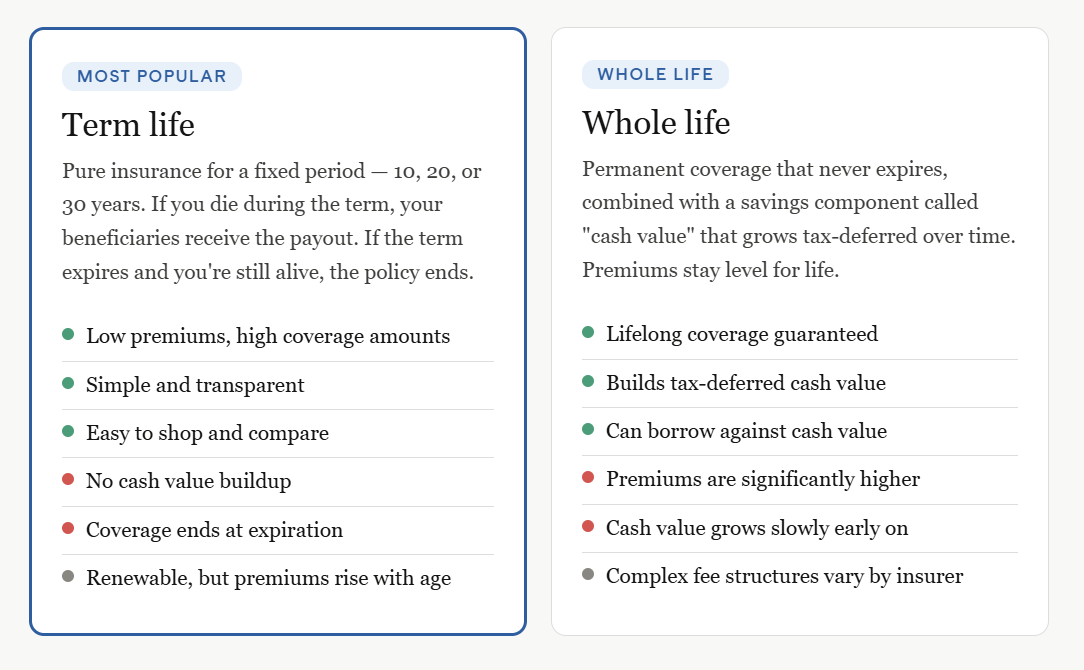

For most people — especially young families and those early in their careers — term life insurance is the financially sound choice. The primary goal of life insurance is to replace lost income and cover obligations like a mortgage, childcare, and debt. A well-sized term policy does exactly that, at a fraction of the cost.

The argument for whole life often rests on the cash value component. Proponents position it as a "forced savings" vehicle. But the math is unfavorable for most buyers: the returns on whole life cash value are typically modest, and the fees embedded in those early years mean it takes a decade or more before the policy breaks even. For most people, investing the premium difference in a 401(k) or index fund will build more wealth over time.

"Buy term and invest the difference" has been the consensus view among fee-only financial planners for decades — and the underlying math still holds. That said, whole life isn't always the wrong answer. There are specific situations where permanent coverage has advantages:

Estate planning for high-net-worth individuals. If your estate will owe federal estate taxes, a whole life policy held in an irrevocable trust can provide liquidity to pay those taxes without forcing your heirs to sell assets. This is a legitimate, widely-used strategy — but it's relevant only if your estate exceeds the federal exemption threshold (currently over $13 million per individual).

Dependent with lifelong needs. If you have a child with a disability or a dependent who will never be fully financially independent, a term policy may not provide enough coverage. Whole life guarantees protection regardless of when you die.

Business succession planning. Business owners sometimes use whole life policies funded through buy-sell agreements to ensure a smooth ownership transition. The tax-deferred cash value can also serve as a liquid business asset.

How much coverage do you actually need?

A common rule of thumb is 10–12 times your annual income — but that's a starting point, not a formula. Add up your outstanding mortgage, other debts, estimated childcare costs through adulthood, and any income your family would need replaced. Subtract existing savings and other life insurance. What's left is your coverage gap.

A 35-year-old in good health can typically get $500,000 of 20-year term coverage for under $30 per month. That's meaningful protection at a genuinely affordable price point — which is why it remains the product most financial advisors recommend as the foundation of family financial planning.

Financial Advisor in Chicago, IL

Stenger Family Office - Chicago Financial Advisors

150 N. Riverside Plaza

Suite 1950

Chicago, IL 60606

(630) 912-8295

Other office locations:Naperville, IL | Houston, TX | Baton Rouge, LA